plasma-gamification

Archit Suthar

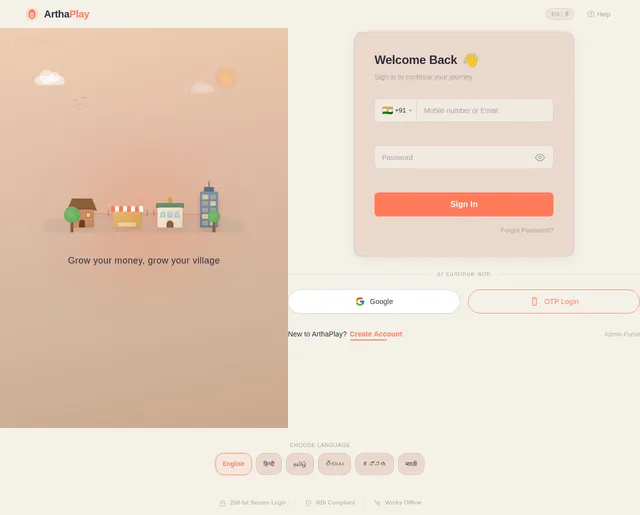

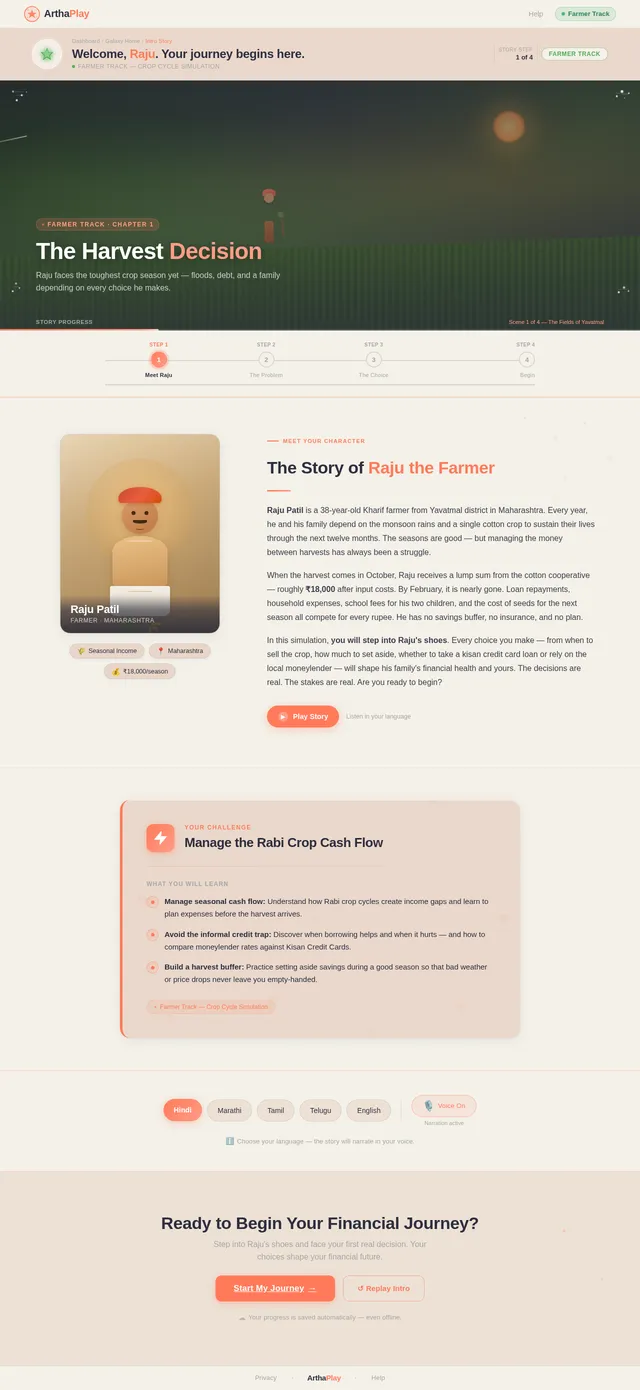

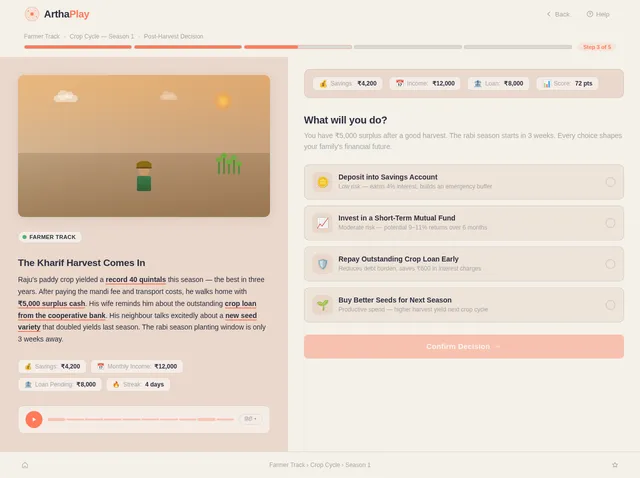

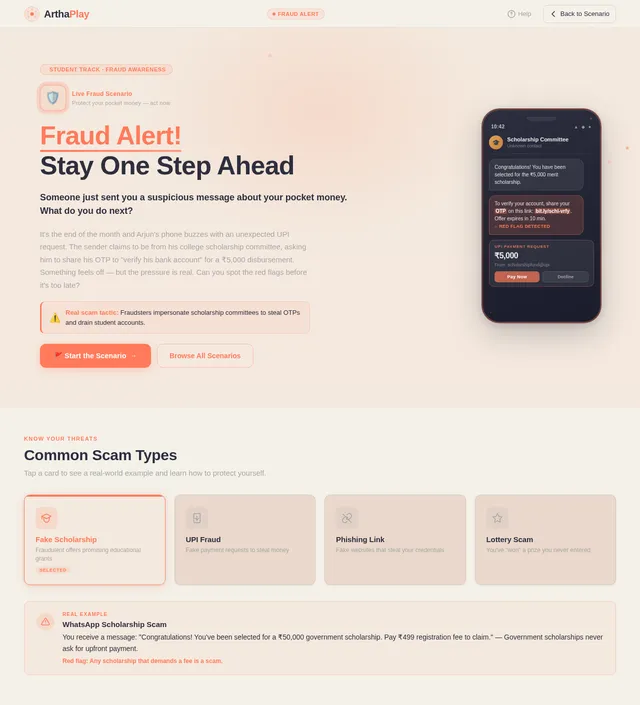

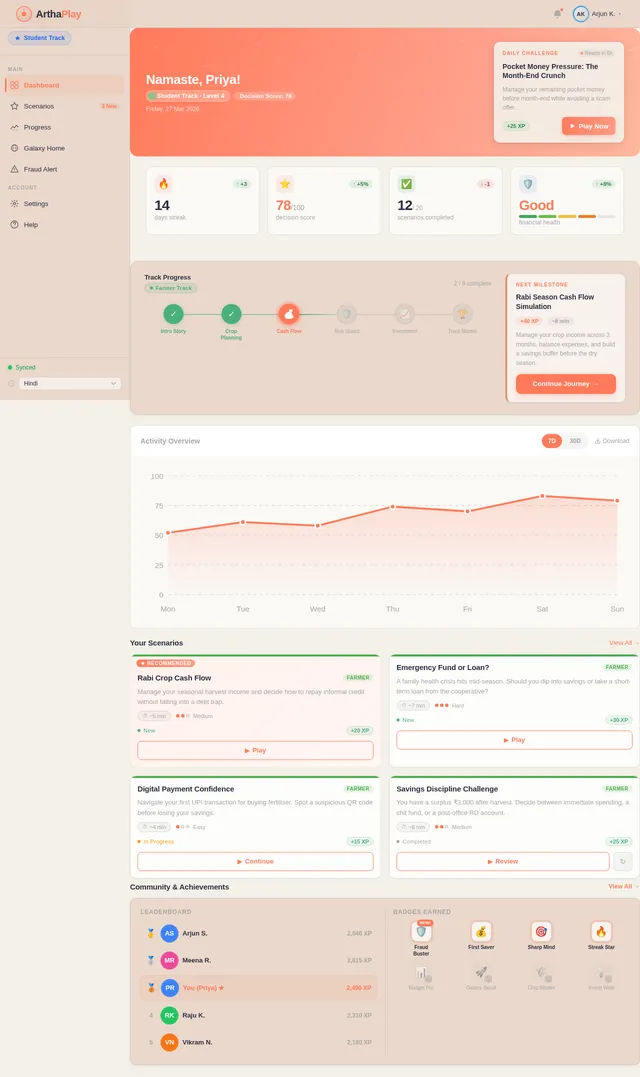

Archit SutharGamifying Financial Literacy for Bharat – Interactive Learning through Play Background Financial literacy is a combination of financial awareness, knowledge, skills, attitudes, and behaviours necessary to make sound financial decisions and ultimately achieve financial well-being. It enables individuals to make informed choices, exercise control over personal finances, avoid financial scams, and confidently navigate evolving financial systems. Financial literacy also encourages saving and investment to manage short-term income fluctuations and achieve long-term goals. Financial well-being reflects the ability to handle unexpected financial events, manage financial stress, and confidently use financial resources. Financial literacy policies and programmes ultimately aim to strengthen this individual financial well-being. Different user groups face distinct challenges. Farmers manage irregular and seasonal incomes with limited access to formal finance. Women encounter gaps in digital, financial, and entrepreneurial confidence. Students are forming money habits for the first time. Young adults face scams, impulsive spending, and weak long-term planning. The Core Challenge This hackathon invites participants to design engaging, context-aware, and behaviour-driven gamified solutions that simplify financial concepts and make them actionable in everyday life. Solutions should move beyond awareness and enable learning through exploration, simulation, and decision-making. Teams are encouraged to interpret the problem creatively, combine or adapt user tracks, and explore ideas beyond illustrative examples—provided the solution strengthens financial resilience and promotes behavioural learning. User Tracks Track A: The Farmer Farmers face financial literacy challenges primarily related to managing irregular and seasonal incomes, meeting time-bound expenses, and coping with uncertainty. Key gaps lie in cash-flow management, savings for lean periods, responsible use of credit, and risk protection. Limited familiarity with formal banking, insurance, and digital payment systems often leads to reliance on informal credit and low preparedness for financial shocks. Strengthening budgeting skills, savings discipline, credit awareness, and risk management behaviour is critical to improving stability and resilience across agricultural cycles. Track B: The Woman Women often manage daily household finances while contributing to income generation, yet face gaps in digital confidence, formal financial usage, and long-term planning. Challenges commonly arise in budgeting across multiple needs, separating household and business finances, using banking and digital payment systems safely, and building savings for future security. Enhancing confidence in financial decision-making, strengthening skills in savings, debt management, and digital safety, and encouraging proactive use of formal financial services are central to improving financial control and independence. Track C: The Student Students are at an early stage of developing money-related understanding, habits, and attitudes. Their financial literacy needs centre on basic budgeting, saving, prioritising needs over wants, and safe digital behaviour. Limited exposure to real decision-making often results in weak behavioural control and low awareness of consequences. Building foundational knowledge, encouraging reflective spending and saving behaviour, and fostering positive attitudes toward planning and discipline are essential to shaping healthy financial habits early in life. Track D: The Young Adult Young adults face increasing exposure to complex financial decisions involving income management, credit use, investments, taxes, and digital financial platforms. Common challenges include impulsive spending, vulnerability to scams, inadequate savings, and weak long-term planning. Gaps are often observed in understanding risk–return trade-offs, managing debt responsibly, planning for retirement, and protecting oneself in digital financial environments. Strengthening decision-making skills, behavioural control, and long-term orientation is key to enabling informed choices as financial responsibilities expand. Functional & Technical Constraints The Rule of Three: Integrate at least three financial themes such as savings, budgeting, insurance, investments, retirement, digital finance, consumer rights, or fraud prevention. Rural-Ready Technology: Solutions must be lightweight, low-bandwidth friendly, offline-capable, and rely more on voice and visuals than text. Behaviour Over Theory: Go beyond quizzes and include simulation or decision-based mechanics with meaningful consequences.

Comments (0)

Sign in to leave a comment

No comments yet. Be the first!